Kalamazoo Resources (ASX:KZR)

Kalamazoo Resources (ASX:KZR)

They've kept a chunk of Kali Metals and optioned Ashburton to De Grey - now what?

Holders of this ASX-listed microcap gold stock have been on quite a ride since IPO, but it seems that the company is finally finding an identity as a ‘project generator’.

Disclaimer: This is not financial advice. At the time of publishing I am not a holder of KZR, but I may (or may not) become one in the future and you should read this as if I am biased.

Contents

Intro

Chart

Financials

History / Projects

People

Where to from here?

Intro

To cut straight to the chase, Kalamazoo Resources (ASX:KZR) has assets that on paper are worth more than double than its current market cap (details below). That’s interesting at the very least.

Stocks in situations like this are not necessarily rare, because not all companies that possess valuable assets actually unlock that value for their shareholders. Assuming the efficient markets hypothesis (noting that there’s a reason this is a hypothesis and not a rule, particularly in microcaps), one could suppose that the market does not currently believe that the value will be returned, and it’s up to the board and management to prove them wrong.

Enter Dr Luke Mortimer, CEO of Kalamazoo, who has a message for you!

How many times can you weave some variation “shareholder value” in 30 seconds into an answer? Dr Mortimer can do it five times!

“Well obviously we’ve just done two major deals. We’re returning money back to the shareholders, and it really fits with our strategy of identifying projects where we think we can add value - doing the work - and then ultimately turning it into shareholder value, whether we monetise those assets, find other partners, or simply go down a development route ourselves. But it’s all just part of our strategy of getting quality projects, enhancing the value of those projects and basically turning that into shareholder value.”

In today’s deep dive, we’ll look at where the company is today, where it’s been, and hopefully that gives you enough to speculate as to the direction of both the company and the share price from here.

Chart

Here we have a tale of two charts - pre and post the last big leg up in the gold price, culminating in it reaching $2069 in August 2020. During that leg up, the share price rocketed (aided by a couple of pieces of excellent news), and it’s been all downhill since then, despite gold currently pushing all-time highs in nominal terms.

Of course, many microcap gold explorers have charts that follow a similar theme, though typically you’d expect more dilution over this sort of horizon. Kalamazoo has avoided a lot (but not all) of this by having had income come in throughout this period via project and tenement sales.

Financials

Shares on Issue/Market Cap

Kalamazoo has 174.8m shares on issue, as well as 1.9m performance rights and 18m options expiring September-November 2025 with a strike prices of 36.5-37.5c. At 9.7c per share, and assuming the options expire worthless, the company has a current market capitalisation of $17m.

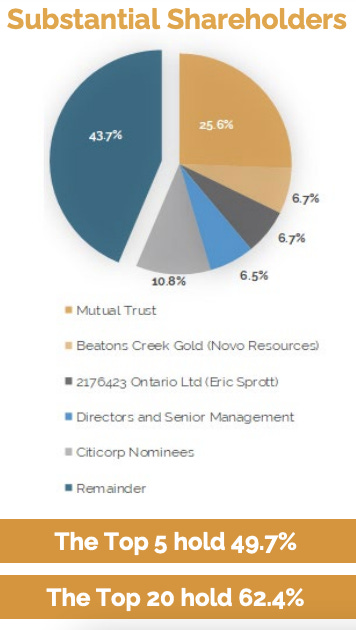

Register

KZR has maintained a fairly tight register since IPO in 2017. The major shareholder is the family of co-founder and Executive Chairman Luke Reinehr with 25.6%. Eric Sprott and Novo Resources have 6.7% each - their strategic stakes being announced doubled the price to ~70c in January 2020.

Value of assets

It’s usually hard to value an explorer’s assets in any concrete way, especially without real geological knowledge, but KZR has a couple that have tangible valuations, which sum to more than double the current market cap.

Kalamazoo owns 20.2% of Kali Metals (ASX:KM1). That stake is worth $13.5m today. They have also just received a $3m option payment from De Grey Mining (ASX:DEG) for a 12-month option (extendable to 18 months) to purchase their flagship Ashburton gold project in the Pilbara for two payments of $15m - one on the exercise of the option, the next 18 months later. For the sake of convenience - discounting for potential to fall through and the time value of money, let’s value that $33m total transaction value at $25m. That gets you to $38.5m for a $17m market cap, assuming the current exploration assets (described below) are valued at zero, which they probably shouldn’t be.

History / Projects

Early days: IPO & West Australian gold projects

Originally co-founded by renowned prospector Denis O’Meara OAM, Kalamazoo listed on the ASX in January 2017 with the Snake Well gold mine in Western Australia’s South Murchison region as its flagship asset. At IPO it sold 30% of the company for $5m at 20c a share.

Snake Well was drilled through 2017 and 2018 before being sold to Adaman Resources (a private company which went into administration in 2021) in November 2018 for $7m, of which $625k was used to satisfy a gold royalty that had belonged to the previous owner, Atlas Iron.

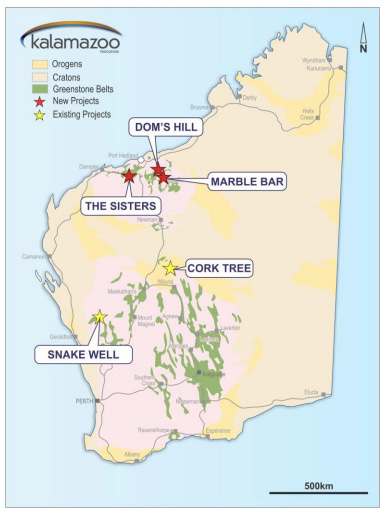

In late 2017 through early 2018, the company optioned, then picked up, three exploration projects in the Pilbara: DOM’s Hill, Marble Bar and The Sisters. Note that the first two of these eventually became lithium assets that went into the recent Kali Metals spin-off, and the latter grew through tenement application and became Mallina West, still held by KZR.

Victorian gold projects

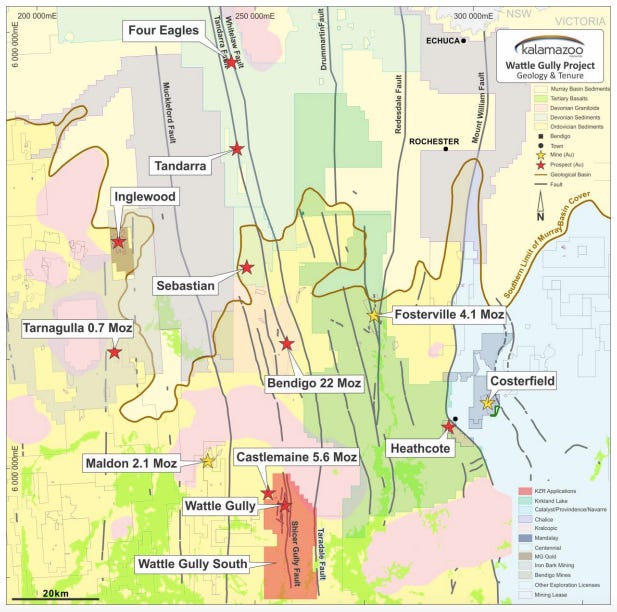

In June 2018, the company announced its first Victorian gold project at Wattle Gully, which would become its Castlemaine project. The ultra-high-grade Swan Zone had been discovered by Kirkland Lake Gold at Fosterville in 2016, and the prospect of similar success at depth in historically productive alluvial goldfields led to Victorian gold becoming a focus for Kalamazoo.

With various acquisitions and tenements being granted, Kalamazoo put together a significant holding of prospective tenements in Victoria, including:

Tarnagulla (2019)

Wattle Gully South (2019, now included in the Castlemaine project)

South Muckleford (2019)

Queens (2020) though immediately JV’d with Novo Resources (ASX:NVO) for $2m in scrip, selling the remaining stake in 2023 to Novo for $1.5m in cash and shares

Myrtle (2021)

Mt Piper (2022)

The first drilling by KZR in Victoria was at the Castlemaine project. A 10,000m diamond drilling program was announced in October 2019, which struck visible gold in December of that year. That was enough to pique the interest of Eric Sprott and partner-in-crime Quentin Hennigh’s Novo Resources, both joining the register in January 2020 with a combined $8m investment, getting 10m shares each at 40c - 24% above the 5-day volume-weighted-average-price (VWAP) of the day, and far above today’s price.

They were looking for Fosterville-like systems.

However, COVID hit, the program ended in April 2020 with less than 5,000m of drilling completed, and the target was deprioritised.

In October 2020, more drilling was announced (4,000m of diamond drilling at Castlemaine, now on the Lightning prospect, and 7,000m of RC drilling at South Muckleford), but only ~45% and ~65% of the drilling was completed. Since then, a planned 2,000m program at Tarnagulla became an announced 800m program, and still hasn’t happened, though is permitted and ready to go.

Aside from that, no other Victorian drilling except for a ~500m reconnaissance diamond drilling program was recently completed at Mt Piper, with assays pending.

Since June 2018, Kalamazoo has drilled only 11,722m in Victoria. While you can’t downplay the value of the essential target-generating, less intrusive forms of exploration, which have been taking place across their landholdings, it hasn’t really got investors’ hearts racing. Why hasn’t the company endeavoured to do more drilling? I suspect some mixture of the following:

conducting exploration and mining in Victoria is generally harder than in other states;

the projects may be seen to have been sufficiently explored to have generated drill targets, and/or corporate interest (as per the Sprott/Novo transaction) - i.e. money could be better spent elsewhere; and/or

the company simply shifted its primary focus to Western Australia when it picked up Ashburton.

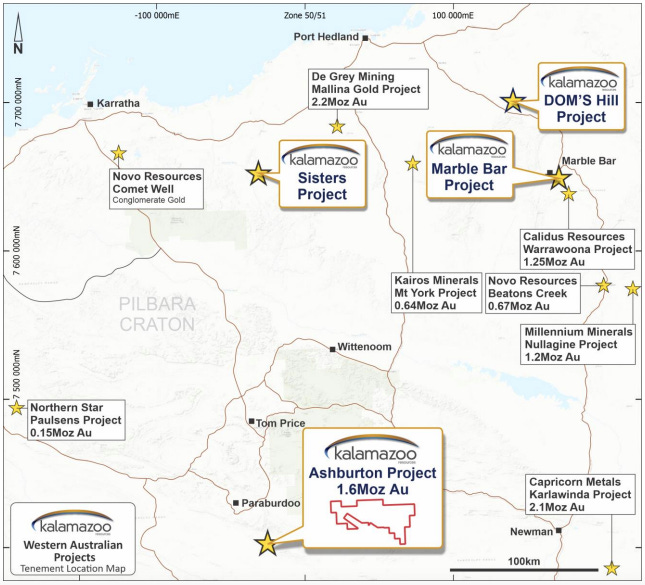

Western Australia: Ashburton

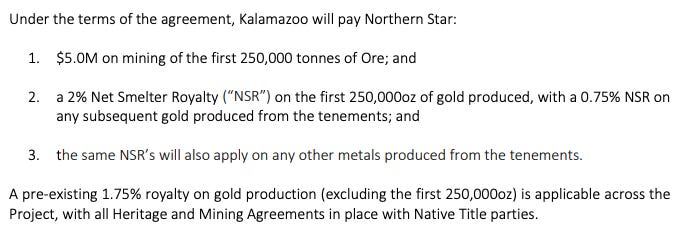

June 2020. You still can’t find toilet paper at the supermarket and gold is breaking out of the $1700-$1750 range it has been in for a couple of months, on its way to $2069. A perfect time to announce the acquisition of the 1.6m oz Ashburton project from Northern Star with all fees dependent on eventual production.

Exploration was to be led by Paul Adams, whose MD gig, Spectrum Metals (ASX:SPX), had that year been taken over by Ramelius Resources (ASX:RMS) for $228m in cash and scrip after he had rapidly drilled out Penny West, also in WA.

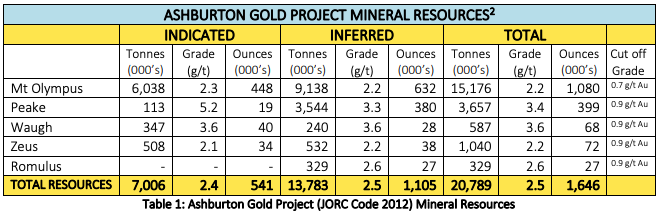

Ashburton was explored for a couple of years before an updated MRE was announced in February 2023 with 1.44m oz (down 200k) but with 911k oz now in the Indicated category (up 68%), and at higher grade overall (up 10%).

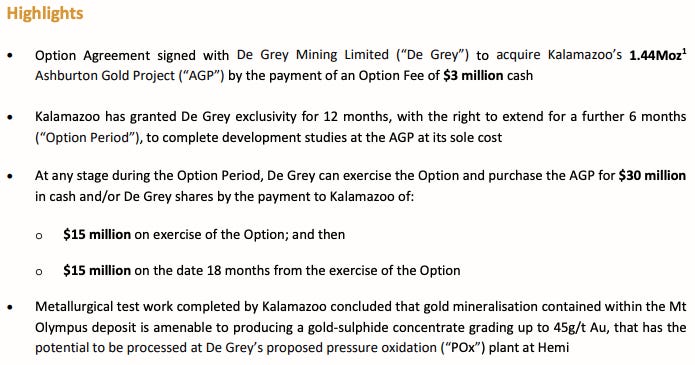

Then just this month De Grey Mining (ASX:DEG) paid $3m to get in there and do due diligence over 12-18 months, with $1m spend required and a $15m+$15m payment structure in cash or shares upon exercise of the option.

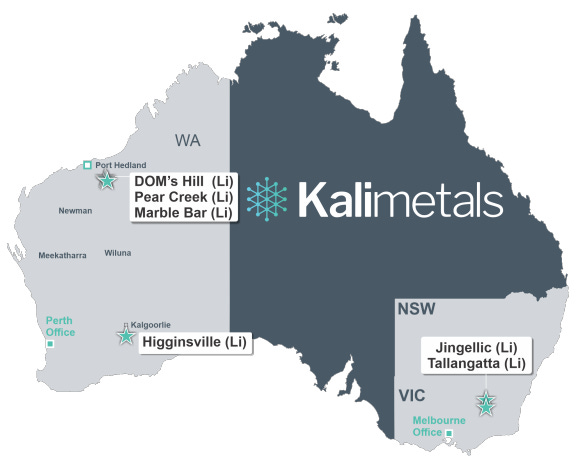

Lithium & Kali Metals

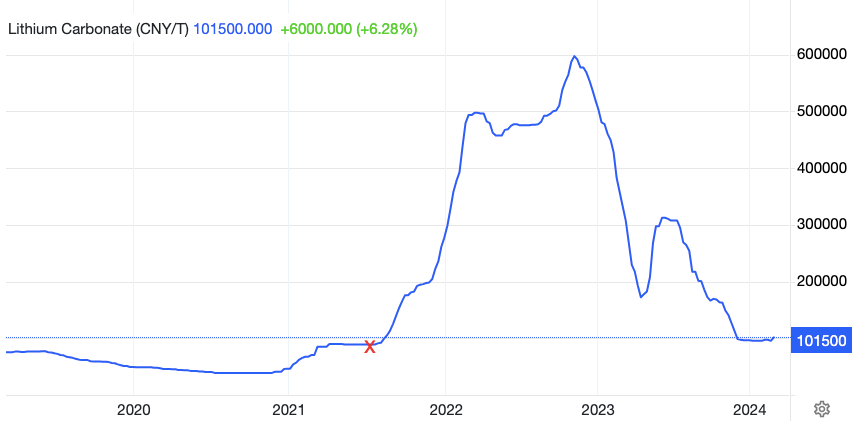

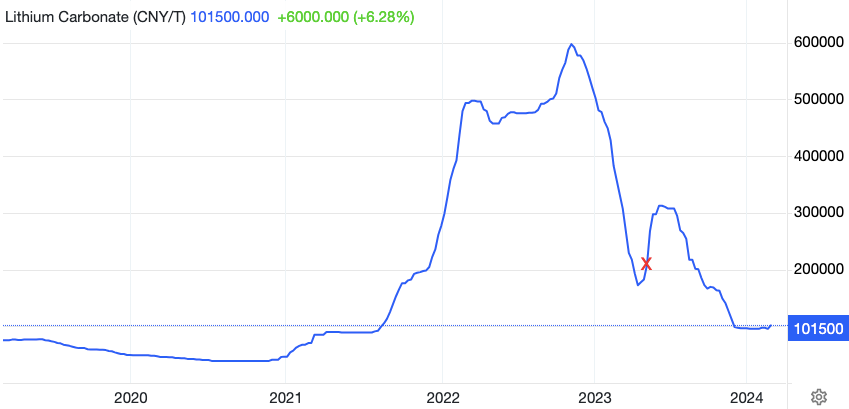

Anyone with even half an eye on ASX resource stocks will be aware of lithium’s wild ride which began in 2021. Kalamazoo’s lithium story starts around about here (the ‘x’ on the chart below), in July 2021, when lithium carbonate prices had started to climb, but before they went completely insane.

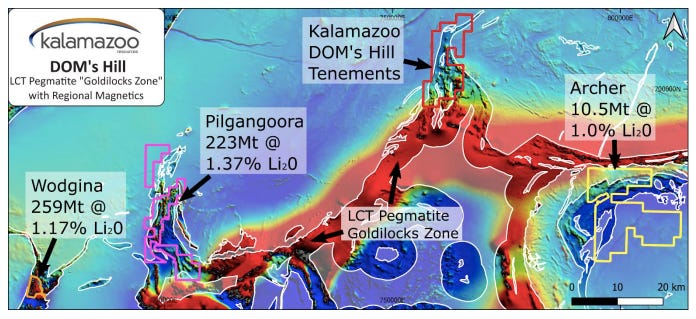

The company announced that their DOM’s Hill tenements were prospective for lithium and that “the project contains a similar geological setting and target host rocks strongly analogous to that of the nearby world class Pilgangoora and Wodgina pegmatite-hosted lithium deposits”. Pilgangoora being Pilbara Minerals’ (ASX:PLS) flagship asset and Wodgina owned 50:50 by global lithium leader Albemarle (ALB:NYSE) and Chris Ellison’s Mineral Resources (ASX:MIN) - more on him later.

In contrast to the pace things were moving in Victoria, the second half of 2021 saw KZR:

pick up the Pear Creek project, situated in between those tenements; and

bring one of the world’s leading lithium producers, Chile’s SQM, into a JV over DOM’s Hill and Marble Bar, which would see SQM sole fund $12m over four years to earn 70% of the projects

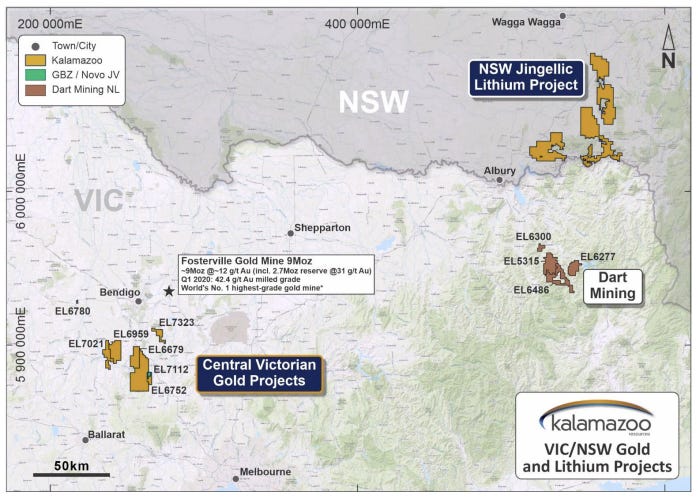

Through the first half of 2022, exploration continued at Marble Bar. In June, the company announced that they had picked up land prospective for lithium in southern NSW, analogous to the Dart Mining’s Dorchap Lithium Project (see image below), which SQM had also entered a JV to earn into.

Later in 2022, Phase 1 drilling was done at Kalamazoo’s JV with SQM, the NSW lithium project expanded over the border into Victoria, and early in 2023, like any listed lithium explorer worth its salt, it announced high-grade rock chip samples at Marble Bar.

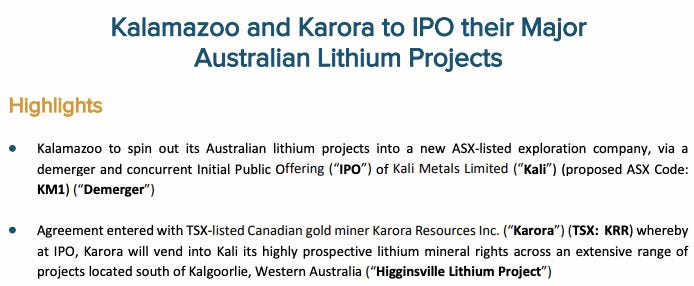

At this point, the company really seemed to have two distinct priorities: the Ashburton Gold Project and the rapid work being done to pull together these various lithium assets. Despite the rock chips*, the market hadn’t seemed to appreciate the lithium side of the business, however, and a spin-off, Kali Metals (ASX:KM1) was announced in May 2023 in partnership with TSX-listed Karora Resources (TSX:KRR).

*I’m kidding, but only sort of! Rock chip sample announcements were all the rage in the lithium bull run of 2022!

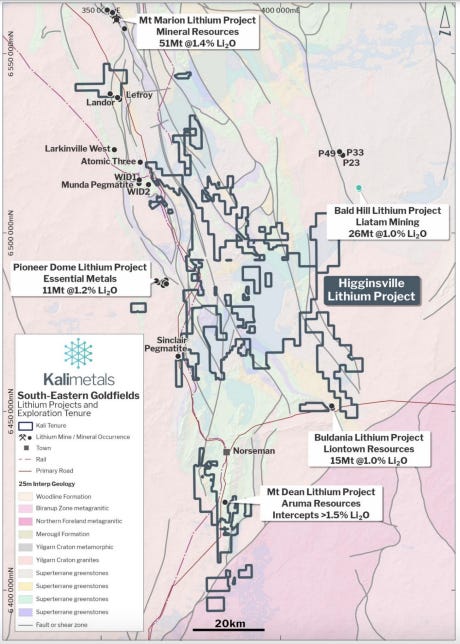

The new entity would have Kalamazoo’s lithium assets (including the JV with SQM) in the Pilbara, the “first mover” play in NSW/VIC, and the lithium rights to Karora Resource’s tenements at its Higginsville project, where it produced around 160k oz of gold in 2023.

The selling point of the Higginsville project was two-pronged: first, it was surrounded by various deposits, most notably Mineral Resources’ Mt Marion Project.

It also had some announcements ready to go, teased with juicy tidbits like this:

The timing could definitely have been better. When the spin-out was first announced in May 2023, interest rates globally had been raised at unprecedented speed, and Australia had seen 11 rate rises in the previous 12 meetings of the RBA. This was (and remains) an incredibly difficult market for exploration companies to raise capital in. Not only that, but the lithium price, despite still being historically high, had unwound at a rapid clip as well.

Fear was misplaced, however. While it took a bit longer than expected, the listing eventually came through in January 2024. Kali had hoped to raise $10 to $12m, and ended up getting $15m.

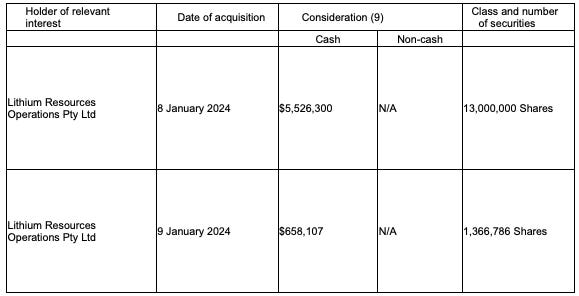

Before IPO, Kalamazoo had 55% of Kali, Karora had 45%. A quarter of KZR’s share was distributed to its shareholders (for every Kalamazoo share, you got ~5.7% of a Kali share, or 1 KM1 for every 17.64 KZR). Post IPO, the company maintains a 20.2% holding in Kali, a holding worth $13.5m at the time of writing (46.5c/share, 3/2/2024).

Lastly on Kali, it’s worth pointing out the frantic trading of its shares in its first few days.

For a company that was available at 25c in the IPO, you can see that the price just took off from day one, hitting a high of 89c on the third day of trading. What kicked that off? Chris Ellison’s MinRes buying 9.97% of the company on market!

And why stop there? After taking a week (assumedly) to contemplate what other unthinkable things he could do after buying 10% of a public company on market in two days, he came back for more, topping up to 14%, this time at a much more leisurely pace, grabbing another 4% in 4 trading days.

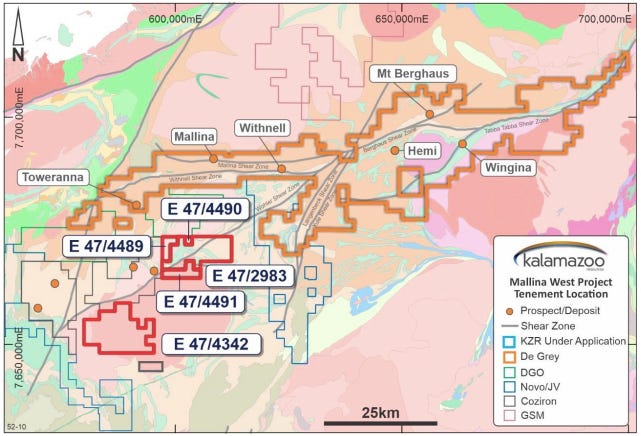

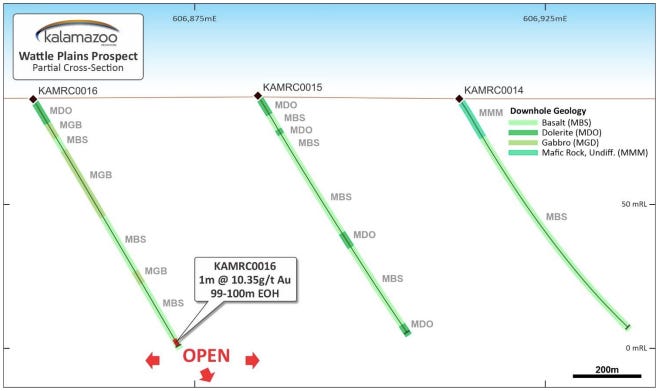

Western Australia: Mallina West

Considering De Grey has optioned Ashburton, and the tenements around Marble Bar have all gone into Kali, the only remaining project that the company has in WA is Mallina West (formerly ‘The Sisters’), which is along strike of, and in the same structural corridor as De Grey’s 10m oz Hemi Project.

The only drilling program here has been a 2,434m, 23-hole RC program in 2022. It didn’t hit anything greater than 1g/t Au except in the final metre of drill hole KAMRC1106, which assayed at 10.35g/t Au.

No further drilling has been done to follow up this result.

People

Luke Reinehr

The co-founder, Executive Chairman and largest shareholder of Kalamazoo. Not much of an online profile, but this short video from 2019 (don’t worry, it’s not in German) sheds light on how he sees (or at least saw) the Victorian gold assets. Given the way the company has added value to Ashburton before selling it off, and packaged up and spun out the lithium assets, I’d be surprised if the Victorian projects weren’t approached in a similar way.

Reinehr was also CEO until only recently, when Dr Luke Mortimer was promoted into the position in January.

Paul Adams

Simply put, Executive Director Paul Adams has technical chops and a track record of success. Took microcap Spectrum Metals (formerly ASX:SPX) from $5m market cap to a $228m sale (mainly in scrip) to Ramelius Resources (ASX:RMS) in less than two years with the Penny West project. Spent 12 years leading research at West Australian broking house DJ Carmichael (since acquired by Shaw & Partners), and prior to that was Chief Mine Geologist at the Granny Smith Gold Mine for Placer Dome, until it was taken over by Barrick in 2006.

When looking for evidence that the potential windfall of $30m is likely to be well spent, having people on board like this provides comfort.

Dr Luke Mortimer

Like Luke Reinehr, current CEO Luke Mortimer doesn’t have a high profile background, but as alumni of WMC, where he spent 11 years in exploration, and having been at Hong Kong-listed multi-commodity producer MMC (HKEX: 1208) for 7 years as Principal Exploration Geologist, leading Australian exploration, it would seem that there is another highly-regarded geo at the wheel.

He’s been with the company since 2019, and started life at Kalamazoo as the Exploration Manger for the Victorian gold projects. He was heavily involved in the technical work done on the KZR assets that went into Kali Metals, which has certainly been a success so far.

Where to from here?

It’s a funny one, Kalamazoo. The company has $3.5m in cash and shares (as of 10/2/2024), plus the $30m revenue (likely) to come from Ashburton and the stake in Kali Metals currently worth $13.5m.

They’ve recently started publicising this value-centric strategy:

At 9.7c, more or less everyone is down on what they bought in at. The Kali in-specie distribution got you about 2.5c of KM1 shares per KZR share at today’s prices. So that helps a little, but not a whole lot at this stage. Aside from that (and the priority offering for KZR holders for the Kali IPO, which was a benefit but only in hindsight - not every IPO goes so well), the value has stayed within the company.

The slide above suggests that the following are potentially on the cards:

capital return to shareholders

in-specie return to shareholders

If any details around these firm up in a way that provided a significant return to shareholders, the share price would quickly get much closer to the current market value of the assets.

If the $30m comes in and management decide to spend the cash on adding value to existing or new projects, I’d be less confident, but still fairly optimistic of a positive outcome.

Reminder: this is not financial advice. At the time of publishing I am not a holder of KZR, but I may (or may not) become one in the future and you should read this as if I am biased.

I publish semi-regular write-ups of different micro-cap resource stocks. If that’s the type of thing you’re into, please subscribe - it’s free!