Alligator Energy (ASX:AGE)

Alligator Energy (ASX:AGE)

Next uranium cab off the rank in South Australia

Contents

Chart

Financials

Key Project

Other Projects

People

Other Considerations

Conclusion

Disclaimer: This is not financial advice. I am a holder of Alligator Energy, so please consider this commentary biased.

Chart

When it comes to ASX-listed uranium juniors, Alligator Energy (ASX:AGE, OTCMKTS: ALGEF) is clearly a market favourite. Well, it was certainly was between March 2020 and March 2022, when it went from a COVID low of 0.1c to a high of 11.5c - a cool 115x. It’s backed off since then, hitting a low of 2.9c in March 2023 before a recent high of 8.3c on January 29th, as the fervour around cuts to Kazatomprom’s 2024 production guidance was at a peak. Today it is 5.8c.

Financials

Market Cap & Share Structure

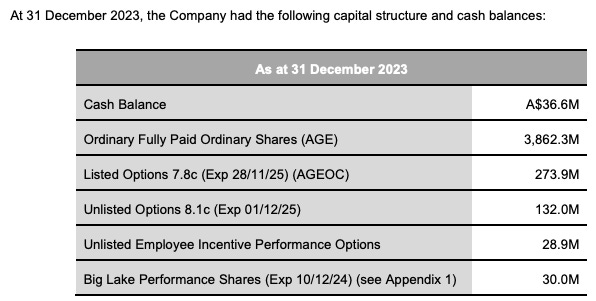

At the current share price (5.8c on 26/2/2024), the company has a market cap of $227m (including Performance Options and Shares), with 405.9m options with an average strike price of 7.9c expiring in Nov/Dec 2025.

Cash Position

Alligator caught many by surprise when they raised $28.76m at 5.2c ($25.5 for sophs, $3.26m in a SPP) in September 2023, despite having ended the June quarter with $18.5, in the bank - a healthy cash balance for an explorer/junior developer. This took the momentum out of the share price upswing that had come off the back of uranium breaking free of its $45-60 range, which it had been in since late 2021.

That said, now, with $36.6m in the bank and with $32m to be raised for the company if the 400m-odd options are converted at 7.8/8.1c by late 2025, the company has a significant runway for resource expansion, feasibility studies and development.

Key Project

Location/Jurisdiction

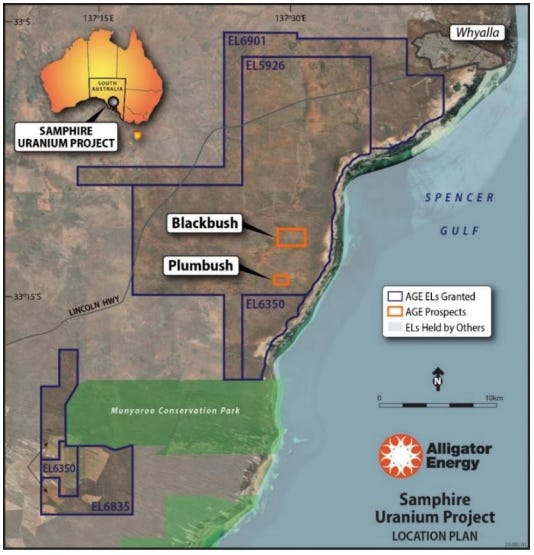

The Samphire Uranium Project is located less than half an hour’s drive from Whyalla, on South Australia’s Spencer Gulf.

South Australia is the home of four operating mines that produce uranium: Beverley and Four Mile (Heathgate Resources), Honeymoon (Boss Energy - ASX:BOE) and Olympic Dam (BHP). It is arguably Australia’s premier jurisdiction for uranium exploration, development and mining, which is valuable considering that other Australian states are far more hostile to the yellow metal.

History

Alligator purchased Samphire in June 2020 with the all-scrip acquisition of the private Samphire Uranium Limited, which had been spun out of UraniumSA (now Everest Metals ASX:EMC) in 2016. When purchased, the project was announced as having 47Mlbs of U3O8 with a cut-off grade of 100ppm.

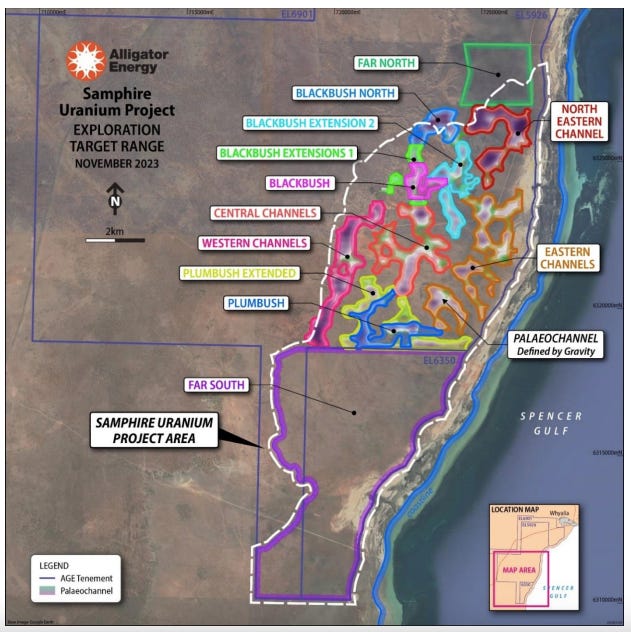

Note that there are two project areas within Samphire, Blackbush and Plumbush, which contributed to this inferred resource. Blackbush when purchased had 32.7Mlbs at 210ppm (JORC 2012), while Plumbush was (and remains) only reported to 2004 JORC standard, and came with 13.9Mlbs at 292ppm.

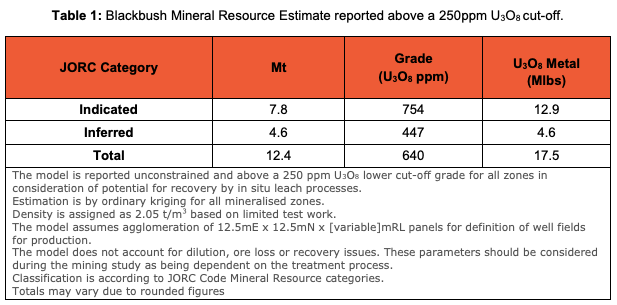

After acquiring the project, Alligator did infill drilling to get enough of the Blackbush deposit to Indicated status that it could be included in a Scoping Study, released in March 2023.

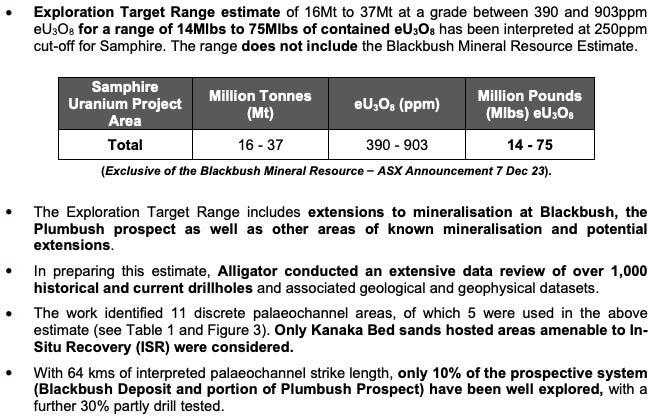

Throughout 2023, further infill drilling was done to enhance the resource and thereby the economics of a revised Scoping Study. Note that a 250ppm cutoff is now used, hence the smaller reported resource.

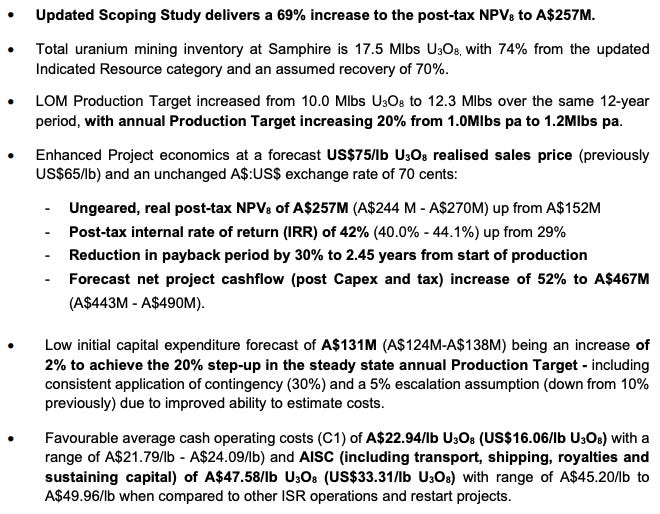

Of course, the real post-tax NPV of $257m is now fairly comparable to the current MC of $227m, even after a 30% fall from the recent high of 8.3c. For such an early-stage project this is a lofty valuation, and the share price is heavily influenced by inclusion in the various uranium sector ETFs. But company-specific factors clearly play a role too, and with a reasonably straightforward path to resource growth defined in an Exploration Target for Samphire, it’s not difficult to see this project vastly increasing in size in the lead up to, and during, the completion of a feasibility study in 2025.

The five targeted areas for drilling are Blackbush Extensions 1 & 2, North Eastern & Eastern Channels and Plumbush. It’s clear, though, just how much more there is to explore.

Next Steps

2024 is a big year for Alligator and Samphire. Resource extension drilling is underway and will continue all year, with a stated aim of enhancing project economics through extending the life of mine, and an updated resource towards the end of the year. The company has applied for a Retention Lease to permit them to proceed with a Field Recovery Trial - essential for all In Situ Recovery (ISR) projects - and while this has been delayed to mid-year, it will optimise economic and technical parameters for a full Feasibility Study in 2025, with the best case scenario for production currently being a H2 2027 production start.

Other Projects

Alligator Energy has several other projects, in both uranium and base metals, and while Samphire is the clear priority for the company, the following projects are advancing to varying degrees:

ARUP: Nabarlek North

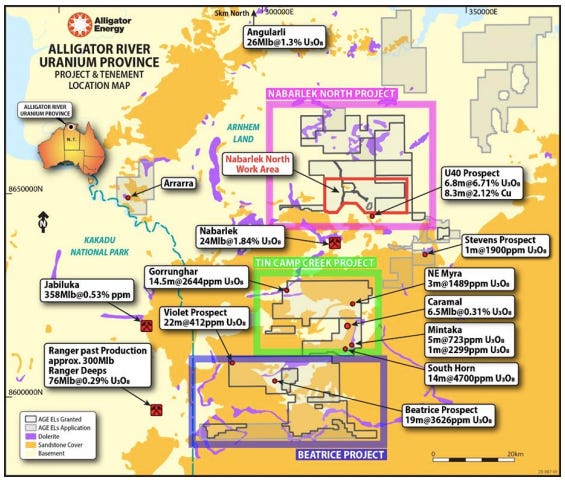

The Alligator Rivers Uranium Province in the Northern Territory is host to the largest, highest grade deposits ever found in Australia, including Jabiluka, Ranger and Nabarlek.

Having listed on the ASX in 2011 with three project areas in the region: Nabarlek North, Tin Camp Creek and Beatrice, Alligator delineated the 6.5Mlb Caramel inferred resource 40km of Jabiluka in 2012. However, it is not seen to have the requisite scale to invest in further, and the company aims instead to explore for a >50Mlb resource elsewhere in its tenement package.

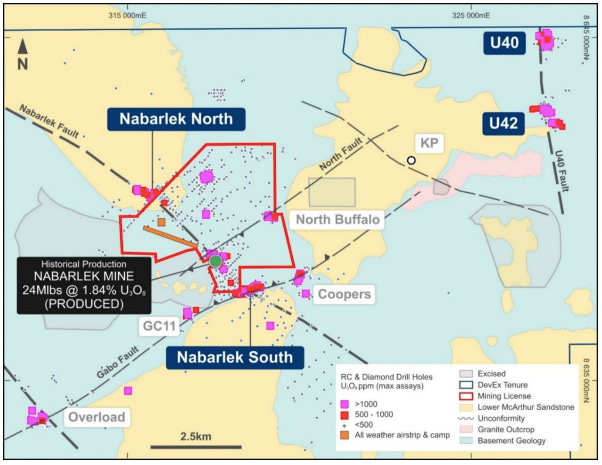

The hunt for a significant greenfield resource is always a challenge, even more so when your primary focus is elsewhere. Fortunately, Devex Resources (ASX:DEV) have discovered their U40 prospect with the standout hit of 6m at 7.6% U3O8 just across the tenement boundary to the south of Alligator’s Nabarlek North project.

Here’s the Devex view from the other side. Note that the fault runs north onto AGE land.

Worth noting as well that Devex is chaired by Tim Goyder, who founded Liontown (ASX:LTR) and Chalice Mining (ASX:CHN) - no stranger to large discoveries.

With Alligator’s maiden drilling campaign only recently completed at Nabarlek North, a new campaign will be defined in Q1 2024 and conducted later in the year.

Big Lake, South Australia

South Australia’s Cooper Basin has Australia’s most important onshore deposits of oil and natural gas, but uranium has never been explored for. However, the company is confident that the geology is analogous to some of the world’s best territory for ISR-compatible uranium deposits:

The company’s latest quarterly suggests a concept-testing drill program is imminent.

Given the scale of the tenement package, there’s definitely the potential for this to become more of a focus for Alligator should results of drilling be promising.

Italian projects

Also with the company since listing, these nickel-copper-cobalt tenements in the northern province of Piedmont - some of which are under a JV which Alligator can progressively farm into - are probably last in the list of priorities for the company. MD & CEO Greg Hall has suggested in interviews that they would be open to partnering with others to unlock value in these assets.

Other Investments - EnviroCopper

In December, the company announced the purchase of an initial $900k, 7.8% stake in EnviroCopper, which is investigating ISR extraction of copper from two projects in South Australia.

With $2.5m of funding from BHP (via its acquisition of Oz Minerals) through 2024, other partners have included CSIRO and the University of Adelaide.

Note that the resources reported below contain only ISR-amenable resources less than 100m from surface.

With a key benefit being the ability to leverage each other’s ISR expertise, Alligator has the option to increase its ownership of the company, and exposure to copper, in a staged process.

People

MD & CEO Greg Hall

Greg Hall is the face of Alligator Energy, having become its CEO in 2018. Key roles prior to joining Alligator were operational mining management roles at Olympic Dam with WMC and at Ranger with ERA/Rio Tinto. After moving into senior commercial roles with Rio Tinto (both in uranium and in aluminium/bauxite), he then led Toro Energy through the previous cycle in uranium from 2006 to 2013, and was the first to get a West Australian uranium mine fully permitted at State and Federal level (Wiluna in 2013).

COO Andrea Marsland-Smith

Andrea Marsland-Smith won AMEC Explorer of the Year in 2008 for the discovery of the Four Mile Uranium Deposit, where ISR mining operations commenced in 2014. She spent 15 years working with Heathgate Resources (owner/operator of Beverley and Four Mile mines) in various leadership roles. She has significant hands-on experience in ISR mining and a track record of uranium discovery in north-eastern South Australia.

NED Peter McIntyre

Peter McIntyre was the founder and Managing Director of Extract Resources, which discovered Husab in Namibia and later sold it to China Guangdong Nuclear Power Corp for $2.2b in 2012. Prior to that had senior roles with WMC.

Other Considerations

Inclusion in ETFs

Alligator is held by various uranium sector ETFs, which drives a significant amount of buying and selling of its stock. These include (data correct as of 24/2/2024):

Global X Uranium ETF (URA): 0.31% weighting, 209.5m shares

Sprott Uranium Miners ETF (URNM): 0.51% weighting, 221.3m shares

Sprott Junior Uranium Miners ETF (URNJ): 1.26% weighting, 97.6m shares

Partnership with Traxys

In 2021, the company formed a strategic partnership with the US arm of Traxys, a global commodities trader. Alligator pays an annual agency fee of USD $125k, and in return gets various benefits from plugging into Traxys’s deep links into the uranium market. These include:

In addition, pre-production finance of up to USD $15m via a secured prepayment for U3O8 will be available to Alligator, and Traxys will backstop initial production to meet contracts if that should be required.

Takeover talk

Here’s a section of an article written by experienced resources sector journalist Barry FitzGerald in September last year entitled: “At 5.5c, could this uranium junior be headhunted by a bigger Boss?”

Famed uranium and natural resources investor Rick Rule describes South Australia-based producer Boss Energy (ASX:BOE) as ‘loved’ by the market, having ridden it all the way from ‘hated’, and regularly praises the management. With well-valued stock and a market capitalisation of roughly $1.9b (as of 26/2/2024), one could see why Alligator might make for an interesting takeover target.

Conclusion

It would appear that Alligator is reasonably valued when compared to its Scoping Study’s post-tax NPV of $257m, with EV of about 0.75x NPV. With most uranium commentary suggesting that the risk of the uranium price is to the upside in the absence of meaningful new supply, it’s unlikely that contracts with floors at or around the USD $75 price used in the Scoping Study are unrealistic - especially so if the company can get into production in 2027 as planned.

In terms of valuation, the company is a long way from production, with company-specific risks, and deserves a discount for that. That said, there’s significant exploration upside, which is highly likely to increase throughput or life of mine in a Feasibility Study, which will most probably give a real lift to the NPV. There’s also the possibility that the uranium term price goes even higher and stays there for a few years, as it did in the 1970s.

I intend to publish semi-regular write-ups of different micro-cap resource stocks. If that’s the type of thing you’re into, please subscribe!